Air, Freight News

New Year and Red Sea offer airfreight market some respite

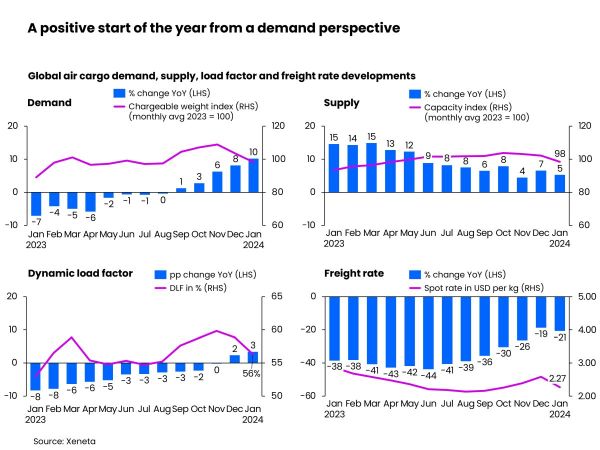

[ February 1, 2024 // Chris Lewis ]Global air cargo volumes rose by a surprise but welcome 10% year-on-year in January as concerns over hostilities in the Red Sea and an early Lunar New Year more than compensated for an anticipated post-Christmas drop in ecommerce traffic, according to the latest weekly market analysis by Xeneta.

With plenty of available air cargo capacity in traditionally a quieter month for demand, however, fuller cargo holds are yet to translate into higher rates. Globally, general air cargo spot rates in January declined -12% month-on-month to an average US$ 2.27 per kg, consistent with the trend in the global dynamic load factor, which dropped three percentage points to 56% versus December. Xeneta’s dynamic load factor analysis measures air cargo capacity utilisation by considering both cargo volume and weight perspectives of cargo flown and capacity available.

Overall, year-on-year growth in global air cargo market supply slowed down in January as much of the missing capacity was restored last year.

Compared to the previous year, January’s global average spot rate continued to show a double-digit year-over-year decline of -21%, although at a slower pace compared to the -38% decline seen in January 2023.

Xeneta’s chief airfreight officer, Niall van de Wouw, commented: “We saw a relatively strong January from a volume perspective, but the market fundamentals have not changed. This is not consumers buying more, it is likely linked to Red Sea disruption as well as the upcoming Lunar New Year and some indicators that the general cargo market is busier than expected. We don’t see this reflected in rates but that’s not surprising in January because there’s not the same pressure on capacity.”

He added: “The situation in the Red Sea has brought nervousness to many supply chains and possibly encouraged some shippers to have a knee-jerk reaction, shifting to airfreight, bringing volumes forward, and securing capacity. However, the consensus seems to be that this will not produce a long-term positive effect on airfreight. Once the initial nerves and uncertainty subsides, stability will return once shippers simply accept that ocean freight may just take two weeks longer, causing the need for airfreight to then dwindle. I’m not hearing it is turning the airfreight market upside down like we saw, for example, during the ports strike on the US west coast.”

Whilst uncertainties due to economic anxiety and geopolitical tensions continue to linger, the air cargo market, van de Wouw said, might be more focused on what happens to ecommerce following the ‘crazy’ air freight volumes online sales generated in the weeks leading up to Christmas. The shrinking German economy, the slowdown of China’s economic growth, and the still-elevated interest rates due to high inflation could also mute global air cargo demand at least in the first half of 2024.

Although the Red Sea crisis will not directly impact e-commerce volumes, it did contribute to some growth in air cargo demand into Europe in January as ocean shipping carriers rerouted vessels to avoid the threat of militia attacks, increasing transit time, driving up costs, and raising concerns over potential container shortages.

With shippers needing to move goods ahead of the Lunar New Year to optimize consumer demand in Europe and boost factory production in China, some of January’s higher air cargo volumes are likely due to some shippers, especially in the apparel industry and producers of manufacturing components, shifting from ocean transport to air.

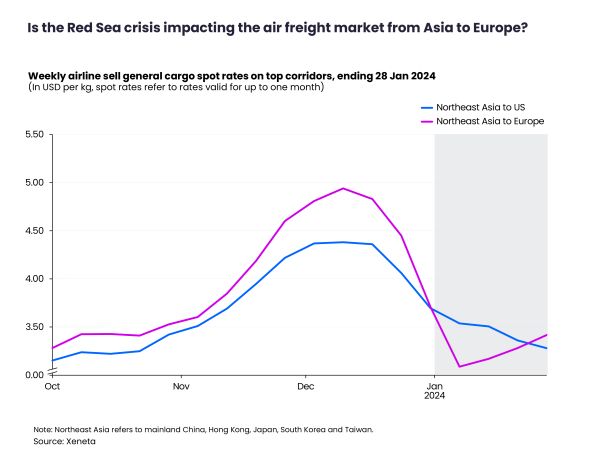

Xeneta observed ‘extraordinary’ surges in air cargo volumes from China and Vietnam to Europe for three consecutive weeks in January, surpassing even their peak season highs. In response to this, the market also saw an increase in some air cargo spot rates. General cargo spot rates from Northeast Asia to Europe rebounded by +11% to $ 3.42 per kg in the week ending 28 January, after reaching their lowest point in the first week of January. Northeast Asia refers to mainland China, Hong Kong, Japan, South Korea, and Taiwan.

This contrasts with the trend of freight rates from Northeast Asia to the US, where general cargo spot rates continued their downward trend since mid-December, reaching US$3.28 per kg in the week ending 28 January, down -7% compared to three weeks prior. This suggests that the demand growth on the Northeast Asia to Europe corridor is more of a spillover from ocean transport rather than actual growth in consumer spending.

While it may have boosted demand for capacity, the Lunar New Year did not manage to push general cargo spot rates from China to the US higher. These hovered around $3.43 per kg in January.

In comparison, general cargo spot rates from Europe to the US remained relatively stable in January at $1.77 per kg, with a slight increase of +4% from three weeks ago. This increase was primarily due to the reduction in cargo capacity, rather than a surge in demand.

“The market remains extremely difficult to predict. Let’s wait and see what happens in February when we might see air and ocean volumes as well as rates fall back if more stability returns to the market. But January was a strong slow month and, after a difficult year, the air cargo industry will not be complaining about starting the year on a positive note,” van de Wouw added.

Tags: Xeneta