Archives

Air, Freight News

Shippers and forwarders learn to commit

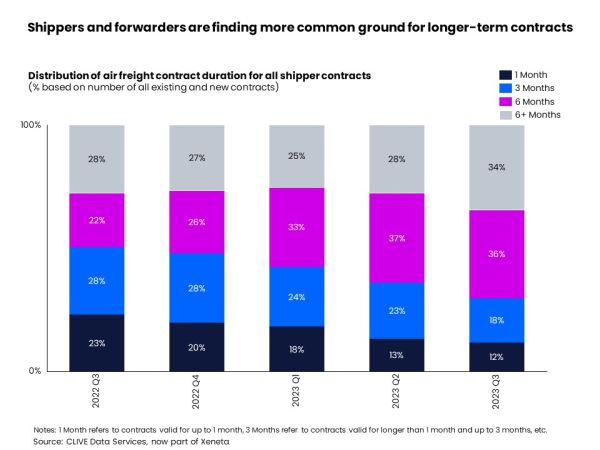

[ October 5, 2023 // Chris Lewis ]Increasing shipper and forwarder confidence in a more stable global air cargo market led to a higher commitment to longer-term freight contracts in September, said Clive Data Services in its latest report, published on 4 October.

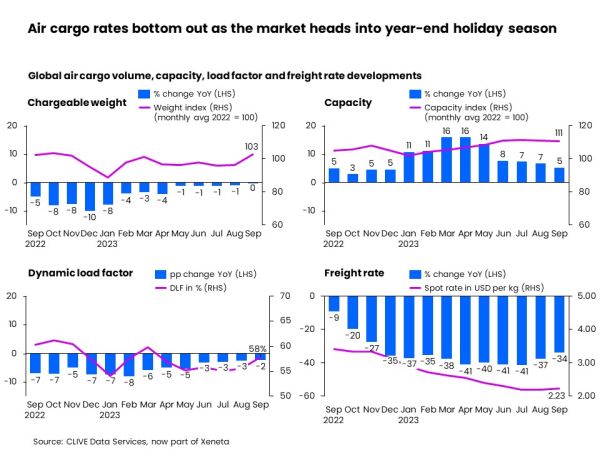

A drop in capacity and traditional month-over-month seasonality pushed volumes up +6%, according to the weekly performance data from the airfreight arm of analyst, Xeneta.

The number of shippers committing to airfreight contracts of over six months in the third quarter 2023 rose to 34% from 28% in the previous three months, Xeneta says, as the industry comes to terms with a new baseline for the general air cargo market.

Chief airfreight officer at Xeneta, Niall van de Wouw, said: “This is not a peak season, it is a sign that airlines, freight forwarders, and shippers are finding more common ground to enter longer-term agreements. … The general air cargo market is entering a new phase where parties are not expecting the market to go much higher or much lower

“We see more longer-term contracts being signed and this only happens when people feel more comfortable about the now and the foreseeable future. It is easier to make a commitment now than when the market is on a sharp downward or upward trajectory.”

The global general air cargo spot rate edged up +2% month-over-month to US$ 2.23 per kg in September, with the growth especially accelerating towards the end of the month. This upward trend continued in the week ending 1 October 2023 as the average global air cargo spot rate rose +10% from three weeks ago.

September air cargo volumes were on par with the same period last year but global air cargo capacity, on the other hand, grew at its slowest pace in the past 11 months. It ticked up +5% from a year ago, but adjusted down slightly compared to a month ago as passenger belly capacity began to be gradually eased out of the market as summer travels in the Northern hemisphere cooled down.

As capacity demand and supply continued to rebalance, the global dynamic load factor, which measures cargo load factor based on both volume and weight perspectives of cargo flown and capacity available, grew to 58% in September, up 2% pts from a month ago. However, the load factor stayed below last year’s level by 2% pts.

Air cargo spot rates on most top trade corridors headed north in September. With cargo rushing out of China ahead of the Golden Week holidays from 1 October, the China to Europe cargo spot rate grew +11% from a month ago to $3.19 per kg in September. Similarly, China to US spot rate rose +9% to $3.63 per kg month-over-month.

Southeast Asia to Europe and to the US spot rates grew considerably, by +22% month-over-month (to $2.29 per kg) and +16% (to $3.14 per kg) respectively. Within the region, Vietnam spot rates to Europe and the US rocketed +54% and +32% to $3.00 per kg and $3.70 per kg respectively. These higher growth ratios are partially due to rates growing from a low base and, on these trades, returning air cargo spot rates to the pre-pandemic levels seen earlier this year.

In contrast, the transatlantic market continued to decline. The air cargo spot rate fell to $1.73 per kg in September, down -3% from a month ago.

The advanced economies remained weak in September. In the US, the Fed’s favourite inflation indicator, core Personal Consumption Expenditures (PCE) prices (excluding food and energy), rose only +0.1% month-over-month in August, the smallest growth since November 2020. However, the overall PCE ticked higher to +3.5% year-on-year in August, which is attributed to wage growth, rebound of commodity inflation, and surging crude oil prices. And it hints that the US economy remains overheated.

The Europe annual inflation rate cooled down to 5.2% in August, with the projected September ratio down further to 4.3%. The reading for the European manufacturing purchasing managers’ index in September of 43.4 continued to point to Europe zone manufacturing activities remaining in contraction.

Niall van de Wouw added: “The global air cargo market is still muted and has been flat at a global level now for three months in a row. September produced no surprises, with traditional seasonality pushing up demand over what we saw in August, and we would expect a similar trend in October with less capacity flying around.

“But in my conversations with shippers, forwarders, and airlines, I still hear very little hope of demand growth before Q3 2024 and for that to happen, we still need to see stronger consumer confidence and economic activity.”

Tags: CLIVE; Xeneta